If I engaged in the drama of all of it, I’d have whiplash from watching the charts by now; demand climbs and then tanks, a new sector comes online, things we thought would never change look like they’re changing. But there was one report that came across my desk really caught my eye. At the end of January, UBS released a new market report entitled “US Real Estate: Rent versus Buy”. They followed that line with the following: “a dramatic turn of events.”

In my opinion, they’re not being hyperbolic. The rent vs. buy analysis is one of those COVID-era conclusions that are defying conventional wisdom. Still, the winner in the rent vs. buy race seems to be concrete, and I agree with UBS—this is an outcome, not a trend.

Rent Is Winning—Why?

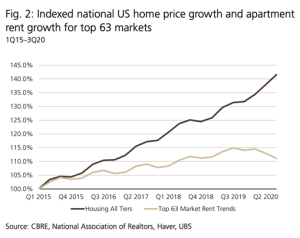

In the figure on the right, you can see the still-climbing home prices as compared to the lower net rent averages through the first two quarters of 2020.

This chart was made using the fully loaded cost of ownership for a single-family home, against the rent payments for an average three-bedroom apartment.

Another figure in the report looks at the rent-buy analysis for 40 of the largest metros across the US, using the same comparison—the rent for a three-bedroom apartment against the cost of monthly home payments for the median single-family home price.

Overwhelmingly, renting was less expensive than owning.

I dug deeper into a detailed market analysis. Nationally, apartment rents declined 3.34%. Meanwhile, existing home prices appreciated 11.96% in the 12 months between Q3 2019 and Q3 2020. This certainly paints an interesting picture, but it’s often more effective to look to local real estate markets rather than considering outcomes at the national level.

Those results surprised me too: New York saw a 6.49% decrease in rent and a 5% appreciation in home prices; Chicago saw a 3% drop and a 10% rise, respectively; San Diego saw a 1% drop and a 12.9% rise, respectively.

The full local breakdown shows that dense, coastal urban markets have seen the greatest spread between mortgage payments and rent payments. This can be explained considering the fall of rent in those areas resulting from job and population migration.

The trends have only continued in this direction, with home prices continuing to rise during COVID-19. And that growing divide is giving rent the overwhelming hand in the rent-buy calculus.

Rent Is Winning—So What?

What Does All This Mean for the Housing Market?

This might qualify as another ‘dramatic turn.’ The mass market shift toward the renting strategy means little to nothing for the housing market. Lower interest rates, available supply, and other favorable trends are enough to caution investors against adopting too much of a bearish approach.

The experts at UBS point to declining mortgage rates as another reason not to be bearish. As mortgage rates continue to hover near all-time lows, they’re offsetting the increase in home prices.

Additionally, a significant portion of the US population is entering their prime homeowner years—44 million people are between the ages of 30 and 39.

Last, the housing sector had a scarcity of new-home construction projects in the decade following the 2008 financial crisis; lower inventories bode well for a competitive market.

It was fun to share in the ‘shock’ of the growing divide between renting and home owning, but a look at the larger picture shows the effects are limited. The housing market remains strong due to a number of factors—low interest rates, declining mortgages, demographic shifts, competitive supply—and I believe rental prices will continue to shift as the long-term effects of the pandemic become clear.

This chapter of US real estate is particularly enticing, full of twists and turns. But it’s always useful to zoom out and consider the larger picture.