COVID-19 has added new twists to longer-term trends in the real estate market, including the effect of student debt on the economy. Some headlines call for doom and gloom, some announce true (or not) loopholes in old systems, and others have championed an optimistic outlook. While these takes come from different minds, everyone seems to agree on one thing: now is the time to consider everything.

Can The Housing Affordability Index be Trusted?

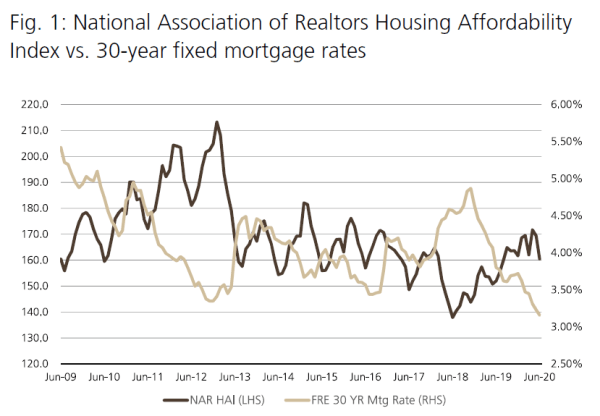

In an August report on housing affordability in the U.S., UBS states that the current HAI sits around 160— housing is widely affordable. It’s an intuitive answer, considering interest rates have dropped significantly. But UBS proceeds to find oversights in the NAR’s considerations, and explains the ways in which the HAI can be deceiving.

One oversight is the lack of attention paid to other costs of owning a home: property taxes, homeowner’s insurance, maintenance, and other general items. Another flaw has to do with assumptions regarding down payments—the NAR assumes a 20% down payment, when many home buyers pay much less. A lower down payment requires new home owners to purchase mortgage insurance or pay premiums, additional costs that are also absent in the HAI calculation.

With these additional costs considered, UBS provides an adjusted HAI which hovers between 100 and 125 under different scenarios. They proceed to detail the median home price compared to median family incomes in 64 different local markets.

Student Loan Debt and Its Effect on Our Economy

Student debt isn’t one of those inevitable home ownership expenses, but it is (increasingly so) a financial factor that nearly every first-time home buyer is contending with. There’s been no shortage of talk regarding the effect of the COVID-19 crisis on the already out of hand state of student loan debt and its effect on our economy.

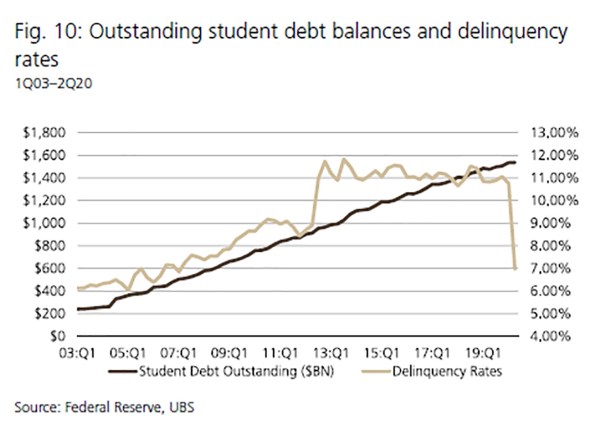

Sitting at a jaw dropping $1.6 trillion, the cumulative U.S. student debt continues to rise — it’s something all young professionals are navigating as they weigh their residential options, and it’s therefore something all investors need to consider as they build their portfolios and predict demand across sectors in the coming years.

Student loans are now the second-largest class of U.S. household debt, and it’s easy to understand how student debt is affecting the housing market. Tuition is only rising.

In March, the Trump administration suspended loan payments and temporarily set interest rates to 0% to offset the economic impact of the corona virus pandemic.

But if we assume rates will return to their prior levels post-crisis, and consider the tidal wave of unemployment and economic insecurity that early-stage professionals will continue to face, the effect of student debt on the economy should be assumed as a long-term force in the real estate market.

Source: UBS U. S. Housing Affordability Report 8/20/2020

Delaying Home-ownership: Student Debt Effect On Economy Overall

When we examine more closely the interplay between student debt effect on economy and the housing market, we find that student debt burdens young professionals from a couple different angles. Not only does it lower their budget for home-ownership, it also often impacts credit scores, and it clearly effects a person’s debt to income ratio.

With a 25% drop in home-ownership rates among younger demographics between 2005 and 2014, it’s clear that these numbers are holding recent graduates back from full market participation. According to Forbes, over 80% of non-homeowners report their debt as a main factor holding them back from buying a house.

A survey by Zillow found 39% of buyers pointed to student debt as an influencer of their delayed home purchase. Like all market factors, student debt shows up in different sectors, in different ways.

While it might slow down a seller’s market, it’s certainly one of the main forces propelling demand across the multifamily real estate sector. Nothing should be considered in isolation—there are a number of factors that might make young professionals favor a more flexible renting arrangement. But the national prevalence of student debt, and the way it affects both credit scores and debt to income ratios, makes it a crucial part of the HAI equation, and it’s not yet something that’s accounted for.

For investors who need accuracy to build and adjust their portfolio, and for potential home buyers who might not see signs of this proposed affordability in their personal books, student debt is a crucial factor, the key to a truer market story.